Are Burial Insurance Costs by Age in 2026 Higher Than Your Family Expects?

If you’re Googling burial insurance costs by age, you’re really asking a deeper question: “What will my family actually owe when I’m gone—and how much do I need to pay each month so they’re not scrambling?”

Funeral prices keep creeping up. The NFDA reports the national median cost of a funeral with viewing and burial is about $8,300, while cremation with a service is around $6,280 based on the latest 2023 data. That’s before any medical bills, credit cards, or travel costs for family.

Burial insurance (final expense insurance) is meant to cover that bill with a small whole life policy that never expires and can’t be canceled as long as you pay. Real policies typically range between $20 and $100+ per month depending on your age, health, gender, and the coverage amount you pick.

In this 2026 guide, I’ll walk you through how burial insurance costs by age really work, show you realistic sample ranges in your 40s, 50s, 60s, 70s, and 80s, and explain how to use those numbers to make a calm, smart decision—without getting sold on teaser rates that don’t fit your health or budget long term.

How much does burial insurance cost by age in 2026?

In 2026, burial insurance costs by age typically range from about $20–$50 per month in your 40s and 50s to $40–$90 in your 60s and $70–$150+ in your 70s and 80s for $10,000–$20,000 of coverage. Exact premiums depend on your age, gender, health, tobacco use, and which company and policy you choose.

What Is Burial Insurance and Why Do Costs Rise by Age?

Burial insurance—often called final expense insurance—is a small whole life policy designed to pay for your funeral, cremation, and last bills. It’s not meant to replace your full income. It’s built to cover that one painful bill your family will face no matter what.

Because burial insurance is whole life, the coverage is designed to last as long as you do. As long as you pay the premium, the policy doesn’t expire, and the death benefit is paid directly to your beneficiary tax-free in most situations.

Costs rise sharply with age for one basic reason: the older we are, the closer we are to a claim. Insurers price burial insurance by age, health, and risk, so a 50-year-old in average health will always pay less than a 75-year-old for the same $10,000 benefit.

How Much Does Burial Insurance Cost by Age in 2026? (Sample Ranges)

Before looking at charts, it helps to see real-world ranges. These numbers are based on current final expense pricing studies for $10,000–$20,000 level-benefit whole life policies from mainstream carriers, not teaser ads.

- In general, younger, healthier, and non-smoking applicants pay less.

- Premiums increase every year you wait to start.

- Women usually pay less than men for the same benefit.

Here are realistic monthly ranges by age band for a non-smoker in average health:

The simple takeaway is this: buying earlier in your 50s or early 60s usually locks in much lower lifetime premiums than waiting until your 70s or 80s.

Want Your Burial Insurance Costs Fully Shopped for You?

See your best options in writing before you ever feel pressured to talk to anyone.

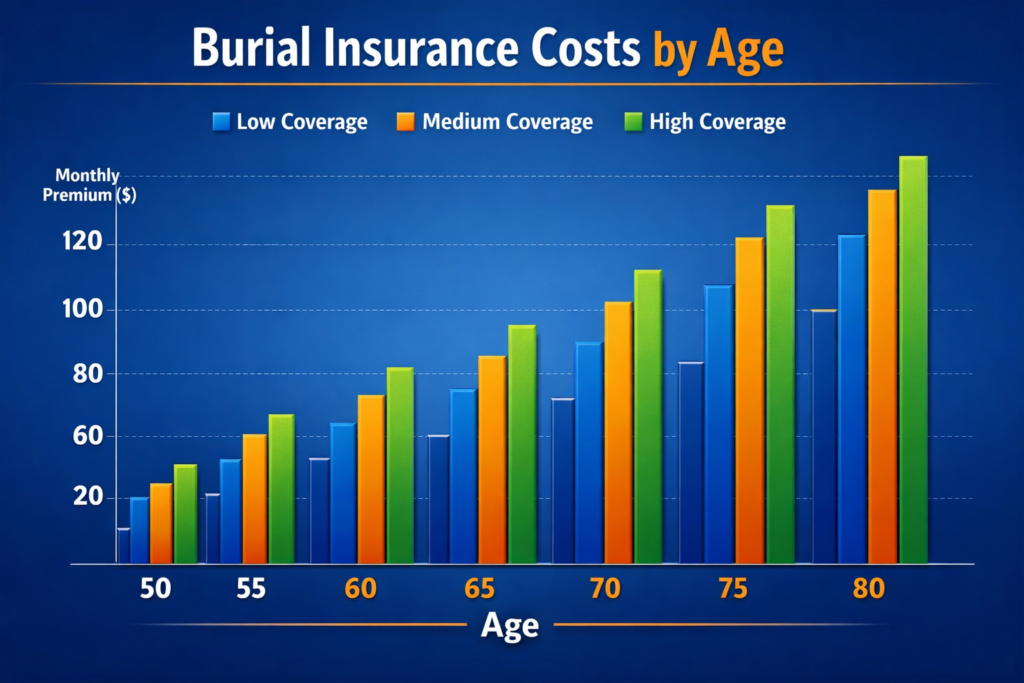

Burial Insurance Costs by Age Charts (Easy Comparisons)

Seeing the numbers side by side makes it easier to judge what’s realistic for your budget. These are approximate, non-smoker ranges for level-benefit whole life with $10,000 and $20,000 death benefits based on current market research.

Burial Insurance Cost by Age – $10,000 Coverage (Estimated Monthly Range)

Before looking at the chart, keep in mind these are blended ranges pulled from multiple sources, not one company’s guaranteed offer. They’re meant to show what’s typical if your health is average for your age.

Burial Insurance Cost by Age – $20,000 Coverage (Estimated Monthly Range)

Because you are doubling the coverage, premiums do not always double exactly—but they do jump. These ranges assume level-benefit whole life, not graded or guaranteed-issue.

For exact pricing, you need a quick health snapshot so a broker can compare multiple carriers instead of one company’s chart.

Let PinnacleQuote Shop Every Major Final Expense Carrier for You.

Answer a few health questions once and get your best burial insurance prices by age emailed and texted—before you ever get on the phone.

What Really Affects Burial Insurance Costs Besides Age?

Age is only part of the story. Two people the same age can see very different quotes because of health, lifestyle, and policy structure.

First, health history and prescriptions have a big impact. Insurers look at conditions such as diabetes, heart disease, COPD, cancer history, and mental health, plus your medication list. Some conditions may still qualify for level first-day coverage, while others require a graded or guaranteed-issue policy at a higher price.

Second, tobacco and vaping matter. Smokers can pay 30–60% more than non-smokers of the same age, and daily cigarette use is usually rated more harshly than occasional cigar use or past smoking with years of clean time.

Third, your state and chosen company influence price. Some carriers are aggressive in certain age bands or states; others are slow or very strict. Shopping only one brand can easily put you in the wrong bucket.

Finally, the type of plan matters:

- Level benefit, first-day coverage

- Graded benefit with a partial payout in the first 2 years

- Guaranteed-issue with a full waiting period for natural causes

Graded and guaranteed-issue plans are there to help people with rough health histories, but you never want to pay extra or accept a waiting period if you qualify for a level plan instead.

Common Questions About Burial Insurance Costs by Age in 2026

At what age is burial insurance cheapest?

Burial insurance is usually cheapest when you buy it in your 40s or early 50s, because you’re farther from a claim and often have fewer health issues. Once you move into your 60s and 70s, each birthday raises the risk for the insurer, and premiums rise quickly for the same $10,000–$20,000 benefit.

How much does a $10,000 burial policy cost at age 60 vs 70?

At age 60, many non-smokers in average health pay about $30–$45 per month for $10,000 in coverage. By age 70, ranges more often fall between $45 and $70 per month for that same benefit. Waiting ten years doesn’t just cost you extra years of premiums—it locks you into a higher lifetime rate.

Is burial insurance more expensive for smokers?

Yes. Smokers and regular nicotine users almost always pay more for burial insurance than non-smokers of the same age. Some companies categorize vaping, cigars, or chewing tobacco differently, but in general, expect smoker rates to be 30–60% higher, and sometimes more, depending on how often you use nicotine.

Is it still worth getting burial insurance in your 70s or 80s?

For many families, yes—if the premium fits your budget. You’ll pay more in your 70s and 80s, but the alternative is leaving loved ones with an $8,000+ funeral bill and no plan. The key is choosing a realistic benefit amount and a level whole life policy you can keep paying comfortably for life.

How Much Burial Insurance Do You Really Need in 2026?

Before you decide whether a quote is “expensive,” you need to know how much coverage actually makes sense. Funeral studies show the median cost of a traditional funeral with burial is around $8,300, with cremation services around $6,280 nationally.

Most people choose somewhere between $10,000 and $25,000 in coverage. That’s usually enough to handle funeral or cremation plus small medical bills and final debts.

A simple way to decide:

- Add up expected funeral or cremation costs in your area.

- Add a cushion for medical bills, travel, and small debts.

- Round up to the next logical benefit amount (for example, $15,000 or $20,000).

From there, you can work backward: if the premium for that benefit doesn’t fit your monthly budget, drop the benefit a step so you get something permanent in place instead of waiting and risking even higher costs later.

Below is an inflation calculator for funeral costs in all 50 states.

Funeral Cost By State

Select a state to view typical costs, then project future costs using a 3% inflation assumption.

“How much burial insurance do I need in 2026?”

How to Get the Lowest Burial Insurance Cost for Your Age Without Getting Burned

The companies who spend the most on TV ads rarely offer the best value. Some heavily promoted plans are actually term policies that increase in price and end at a set age, even though they’re marketed like permanent burial insurance.

To keep things simple and safe:

- Focus on level whole life final expense policies like Mutual of Omaha rate chart—premiums never go up, coverage never expires as long as you pay.

- Avoid offers that sound like “$9.95 covers everyone,” or “no questions asked” when you’re still healthy enough to qualify for better rates. Those often have limited benefits or waiting periods that don’t show up in the headline.

This is exactly where an independent agency like PinnacleQuote earns its keep: instead of just quoting one brand, we compare multiple top final expense carriers for your age, health, and state so you see, side by side, which companies are truly competitive for you—not just in a generic chart.

FAQ

With true final expense whole life, your premium is locked in at the age you start and does not increase each year. Costs only rise if you wait to buy. If a company shows a rate that goes up over time or ends at a certain age, you’re looking at term insurance, not final expense.

Yes. Adult children commonly buy burial insurance for parents to protect the family from sudden funeral costs. The premium is based on your parent’s age and health, and your parent must consent to the policy, but you can own it and pay the premium yourself.

Typically, women pay less than men for the same burial insurance amount because they tend to live longer. Charts that show one price regardless of gender are either averaging the two or using teaser pricing; actual underwriting almost always differentiates by gender.

If the “ideal” benefit is out of reach, it’s usually better to start smaller with a permanent policy you can afford. You can always add coverage later if your budget improves. Leaving your family with $8,000 of coverage is better than leaving them nothing and hoping they can crowdfund your funeral.

Yes. Beneficiaries can use the tax-free death benefit for medical bills, hospice expenses, travel, or small debts in addition to the funeral itself. As long as premiums are current and the claim is valid, the insurer pays the lump sum and your family can decide how to allocate it.

Related Articles

Conclusion

When you break it down, burial insurance costs by age are really the price of certainty for your family. Costs start low in your 40s and 50s and climb steeply in your 70s and 80s, but the bill your loved ones will face for a funeral keeps rising either way.

If you want to make this simple and avoid the noise:

- Let an independent expert quietly shop multiple carriers using your real health profile.

- Focus on level whole life final expense that never goes up and never expires.

- Choose a benefit that covers the basics and fits your monthly budget today—not a fantasy number that keeps you from starting at all.

See Your Best Burial Insurance Options Before You Ever Pick Up the Phone.

No call centers. No bait-and-switch teasers. Just fully shopped rates by age, delivered by a PinnacleQuote expert.

More Life Insurance Resources

- Annuities & Retirement Income

- Business & Key Person Life Insurance

- Final Expense & Burial Insurance

- High-Risk & Medical Conditions

- Informational

- Life Insurance

- Life Insurance Companies & Reviews

- Life Insurance Guides & FAQs

- Senior Life Insurance

- Term Life Insurance Quotes, Rates & Guides | PinnacleQuote